MV #007: The most important Salesforce meeting you missed at Dreamforce unpacked.

MV #007: The most important Salesforce meeting you missed at Dreamforce unpacked.

Lessons, stories, observations and analyses on software sales, building companies and creating customer value.

Read time: 9 min

👋 Hi there, happy Sunday!

Got a special topic for this edition of More Value. After two pandemic years, Salesforce has put on a great show in San Francisco for its customers, partners, and …

… investors.

Yes, Salesforce executives host investors every year to share their business perspectives.

This is a must-read for everyone who is building a software company or working in the B2B software industry.

There’s so much to unpack about what a best-in-class SaaS business does to stay an industry leader for almost 25 years since it launched.

✏️ I’ve listened to the executives present and summarised key points for you.

🥞 Sunday Deep Dive

Salesforce Investor Day 2022

This was the agenda. We’ll unpack the most important bits.

Session 2 - A View from Our CEOs

Salesforce will be a $31bn ARR company by the end of the fiscal year.

A big investment focus is on data residency. The ability for customers to host data in different locations and jurisdictions around the world. The project is called Hyperforce.

👉 My take: This speaks to the increasing trends of data privacy. Startups better listen. If Salesforce hosts its data in the EU, you should too. Otherwise, European customers will not want to buy from you.

Many differentiators called out by the Co-CEOs follow the principle “the whole is greater than the sum of its parts”, which makes the platform sticky.

👉 My take: This also means that many capabilities might offer opportunities for startups to plug gaps within the different products. As long as you deeply integrate with Salesforce, and provide a seamless experience, you can win against the incumbent, Salesforce functionality.

Bret Taylor, Co-CEO

“The biggest obstacle to our growth was not our technolgoy, our customer engagement but the talent to deploy Salesforce.“

The biggest roadblock to unlocking value for Salesforce is not Salesforce technology. It’s the ability to deploy the technology successfully. There is a huge talent gap among many software companies. There are not enough Salesforce consultants. Let alone specialists like CPQ.

But at least Salesforce has a path to train them through Trailhead and other means.

👉 My take: If you are building a company right now, think about the ecosystem early. Ecosystems are a differentiator. As early as possible think about how you can open up your product to partners, users and everyone else to sell, implement and maintain. There are a ton of startups that start out with hacked-together backends where later you need massive amount of engineering resources to make the admin capabilities customer-facing.

Marc Benioff, Co-CEO

“We’ve done a really good job of making the products work together. […] We see more and more customers want the platform.“

Session 3 - Finance Presentation

Amy Weaver, CFO

“We have an incredibly large and expanding TAM. […] This is true regardless of the state of the economy.”

The main growth pillars are geographic expansion, industries and building a 360 platform.

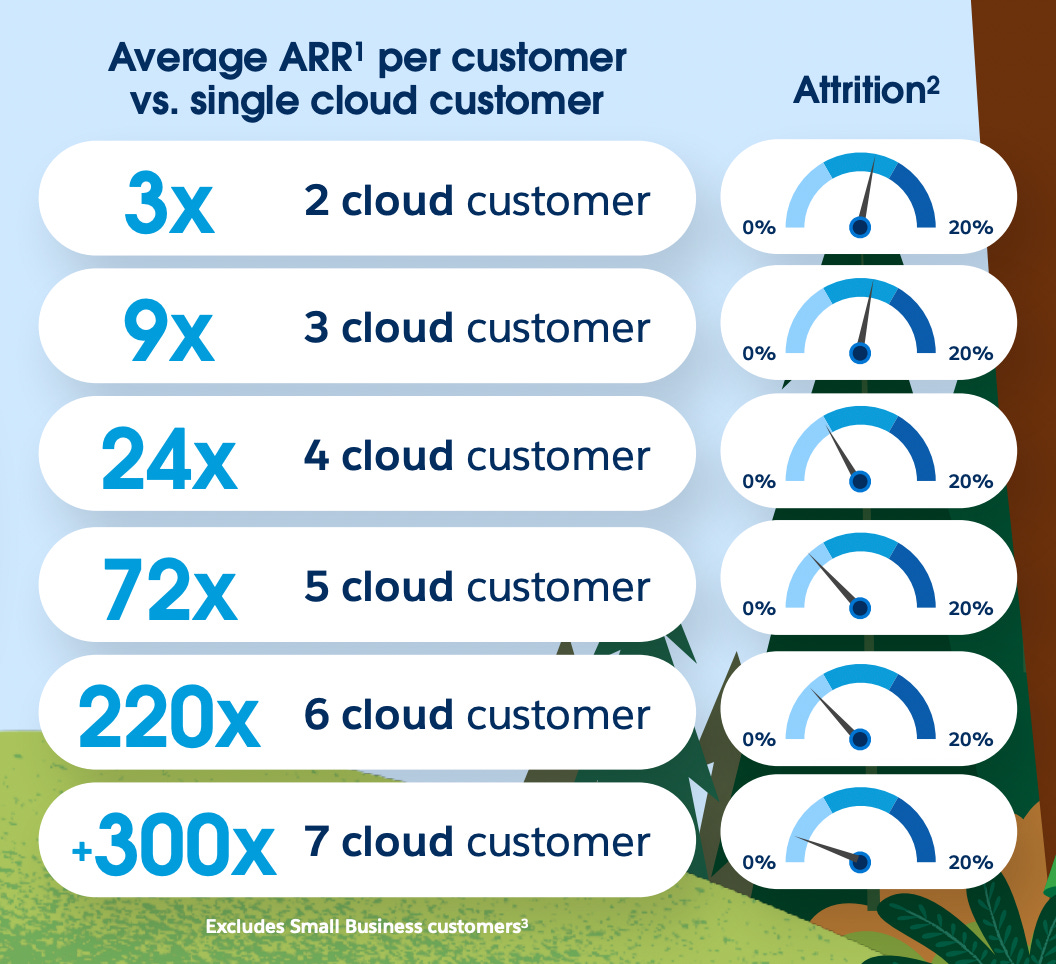

If customers use more clouds, they over-proportionally spend more time on Salesforce.

👉 My take: I’m curious if that is a lock-in too. Salesforce can exert much supplier power if you run your entire business on Salesforce. I wonder if the multi-cloud trend will continue in 2022 or if we’ll see a reversal. Today, it’s much easier to rip-and-replace products than it used to be, thanks to cloud infrastructure and real-time APIs.

The more products someone uses, the less churn.

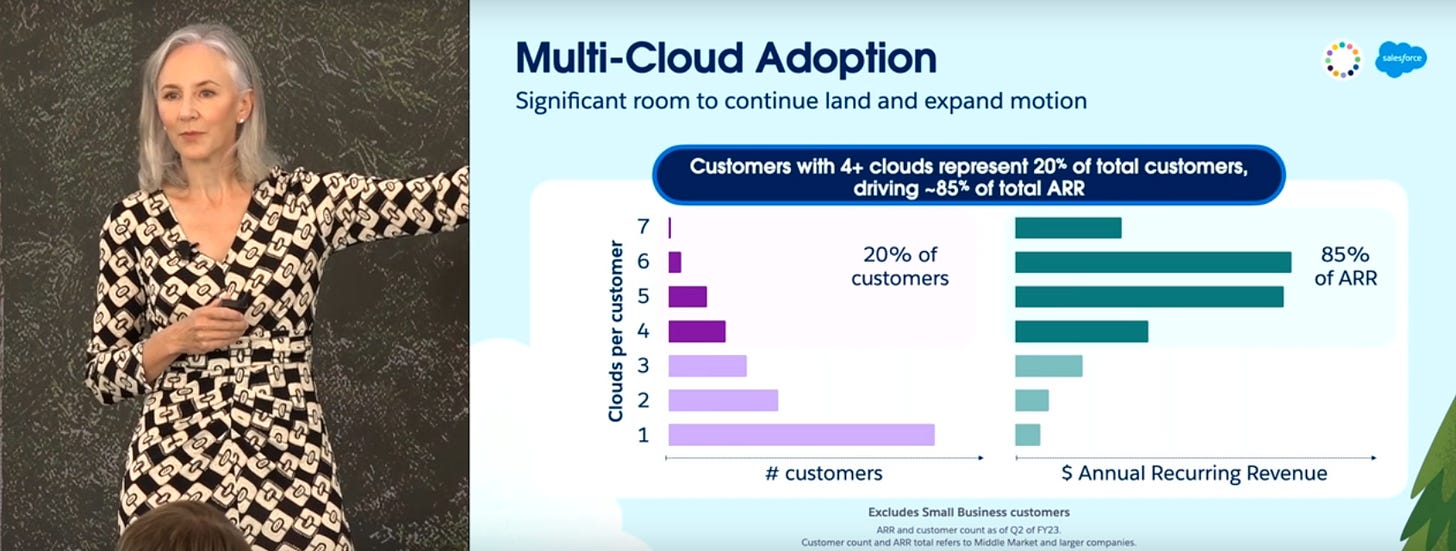

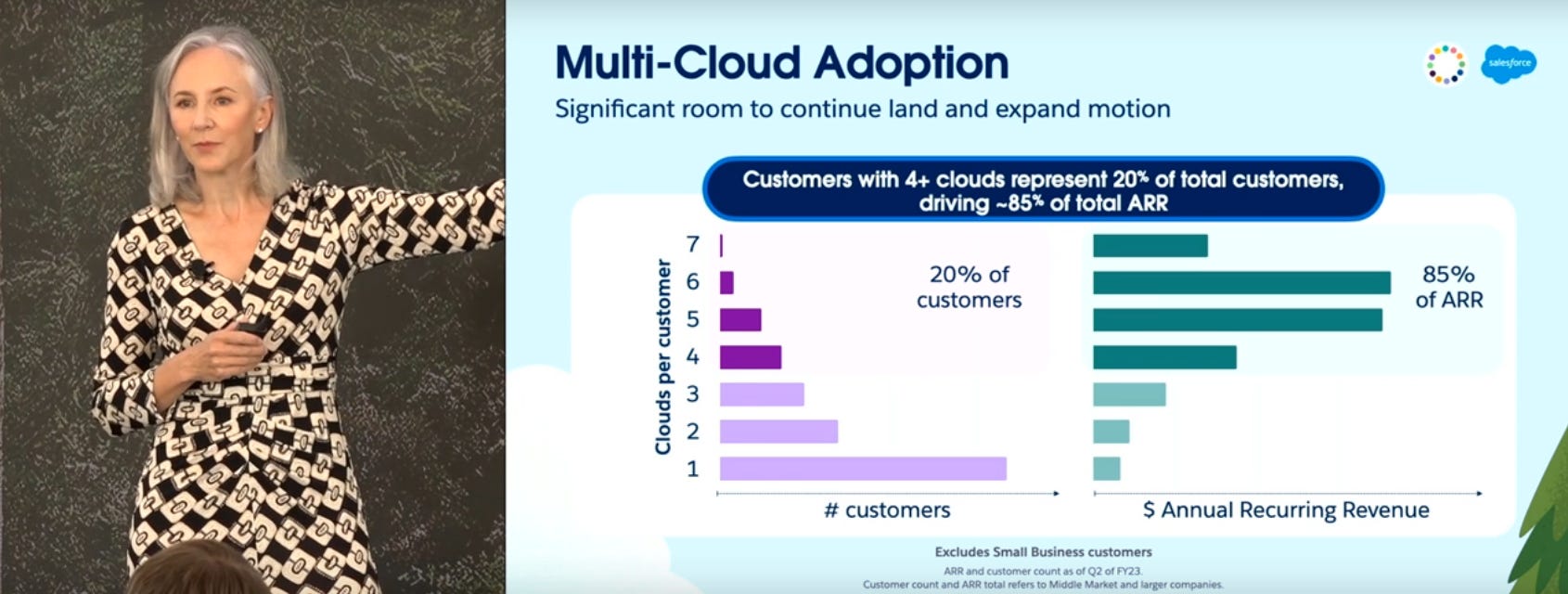

Land and expand is the key to unlocking growth with little effort. The more clouds you sell the more money Salesforce makes. Interestingly, 20% of customers contribute 85% of ARR.

In industry solutions, Salesforce can charge 30% higher ASPs and has ~2% lower attritions.

👉 My take: These solutions are so tailored and integrated that they become sticky from the start. Industry solutions also overcome one of Bret’s points that he mentioned at the start: the talent gap. By productizing Salesforce configurations, the gap can be reduced.

The company essentially bundled together what services companies implemented for industry-specific needs using Salesforce’s vanilla solutions. Industry clouds accelerate revenue, create stickiness and reduce partner dependency.

Enjoy what you’re reading? Consider subscribing and following me on LinkedIn.

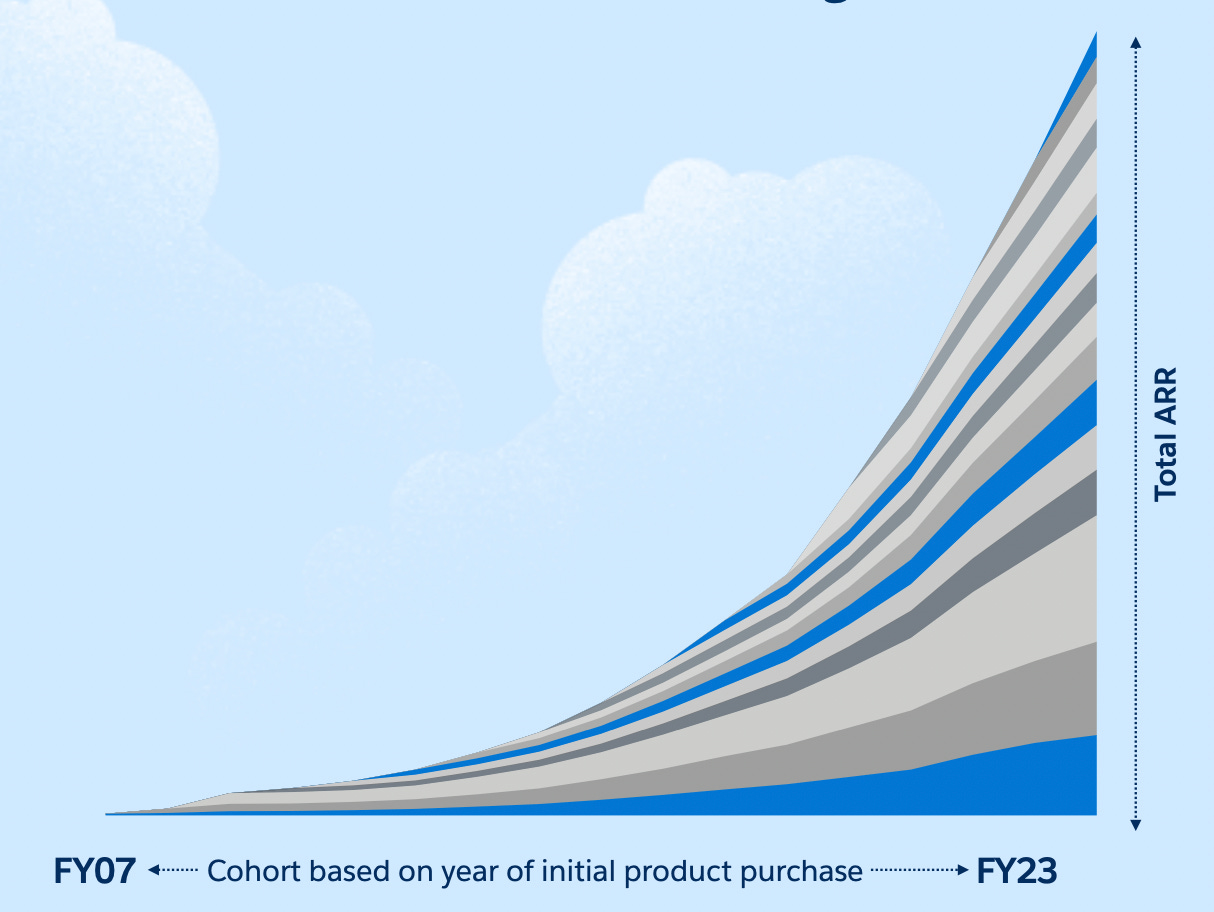

The beauty of multi-product, land & expand visualised.

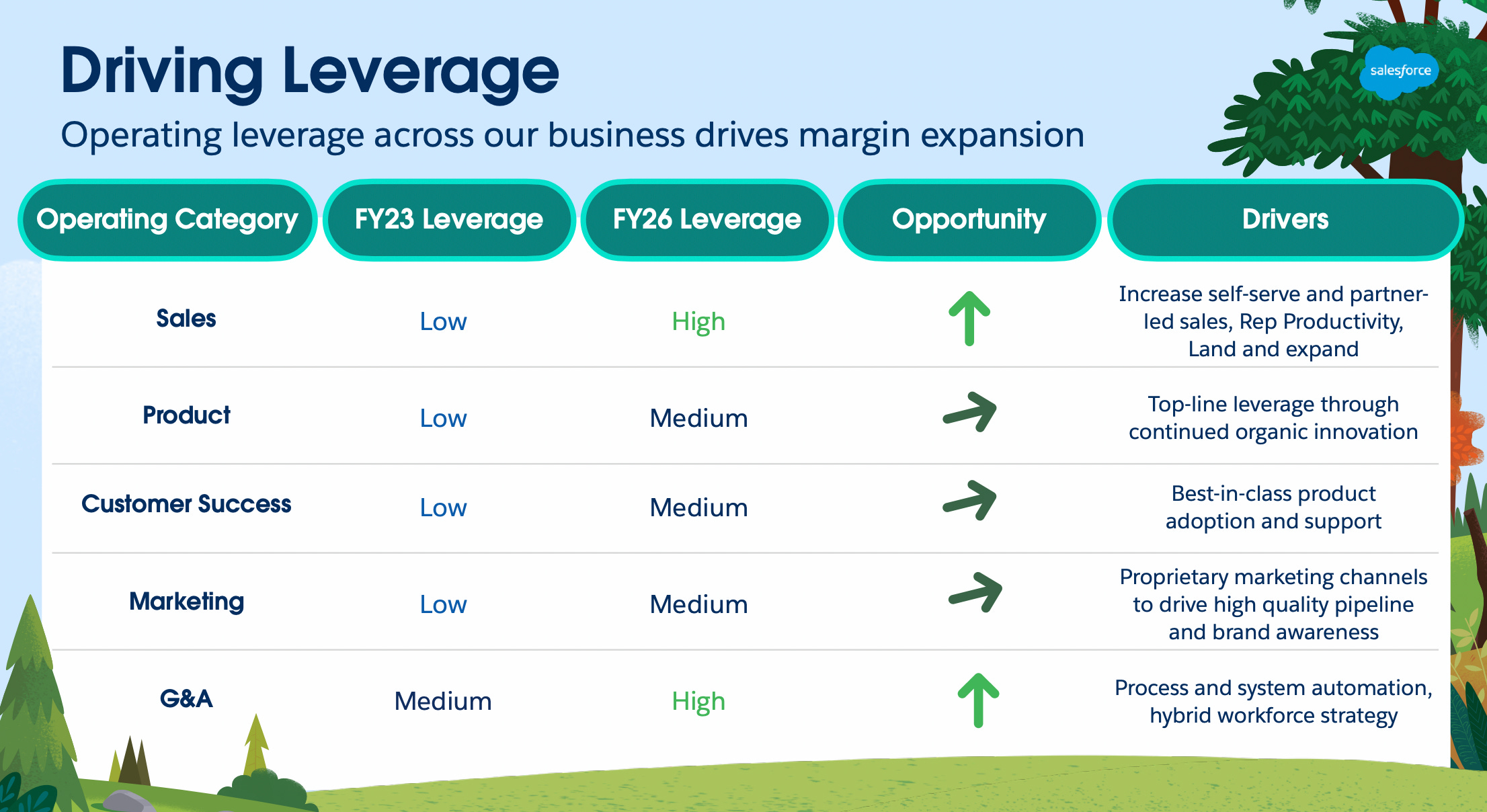

What is Salesforce doing to increase sales productivity?

Diversification of channels by opening up more to partners and enabling self-serve.

Enable sales reps with better support and automation.

Salesforce wants to improve margins further with the below tactics.

👉 My take: Salesforce will be much tighter on expenses, hiring and other spend. Overall, the party times are over, and the company will scrutinise the ROI of every investment.

Session 5 - Customer 360

Genie, it’s Salesforce’s new real-time CRM. Makes me wonder what kind of CRM we’ve used so far.

👉 My take: Genie is an incognito acknowledgement that data is not real-time and stored in disparate silos even within Salesforce clouds. Customer 360 has been a theme for years but seems like a nirvana still.

Salesforce failed to create a single source of truth several times. Time will tell if this time round will work. The competition is tough. Segment, mParticle and Adobe have offerings that do exactly what Genie is supposed to do.

David Schmaier, CPO

“This [Genie] is the holy grail of CRM.“

Parker Harris, CTO & Co-Founder, talked about how Genie can get live data into lightning components in Salesforce and show in real-time what users on a website are doing if you’re a customer service rep, for instance.

The partnership with AWS has expanded. Salesforce is deploying to the public cloud more. The trend is also increasing with GCP and Alibaba. Over time, this should help reduce infrastructure costs and improve margins.

Notably, there was not a single mention of Microsoft and Azure.

Slack is being integrated more deeply with Quip.

👉 My take: Slack + Quip is a half-hearted attempt to use very expensive acquisitions. Quip was probably Salesforce’s most expensive acquihire. Marc likes Bret, and through the past few years that have shown as Bret ascended to be Co-CEO. The product itself is mediocre and has little room amongst all the other players in the office productivity category.

Session 6 - Executive Q&A

Brian Millam, COO (all Sales & Customer Success)

“We see a very strong demand environment. […] There are changes in our GTM around enablement to justify business value.”

Analyst: What are you hearing from customers?

Bret Taylor, Co-CEO

“The scrutiny we see from customers is to drive time to value. […] Ensuring there’s a very well articulated ROI for every technology investment our customers are making.”

Salesforce is the ultimate vendor that can drive technology consolidation.

Automation, intelligence and real-time all drive cost savings. That explains the Salesforce investment in Flow (automation) and other parts of the platform.

Industry clouds help Salesforce get to value faster.

Bret Taylor, Co-CEO sees that self-service can improve through PLG. Traditionally, Salesforce is sales-led, and self-serve has been rather new.

Salesforce has not historically leveraged re-sellers. They might invest more in that GTM motion soon.

Salesforce invested heavily into their GTM functions for industry clouds, more than any other part of the business.

The average Salesforce contract length is 2.4 years, according to Bret Taylor.

Salesforce will invest more in self-service, product-led growth and anything that can reduce the cost of sales as the company aims to improve margins over the next years.

Bret Taylor, Co-CEO

“Small transactions should not need a direct sales interaction.“

ℹ️ Full presentation available here. Recordings are here.

Can Salesforce pull a rabbit out of a hat? Media reactions.

Protocol reported (here) scepticism on the future growth of Salesforce.

“I don’t see how they hit that $50 billion … It’s just not gonna happen,” said Guggenheim Partners analyst John DiFucci. “We can’t get there. I wish.”

There are serious questions about Salesforce’s future growth and how it’ll create a cohesive suite of products. Normally, Salesforce’s M&A machine is very efficient and whilst that’s been the case historically, it seems that signs of a slowdown are showing post the acquisition of Slack.

But the price point may not have been a sticking point if the performance was different. Slack, for example, expected to hit $1.6 billion in sales in FY 2023 without the Salesforce deal, according to a regulatory filing. Now, Salesforce is expecting Slack sales to reach $1.5 billion for the year, per its recent earnings report, indicating that Salesforce hasn’t actually made much of a difference.

👉 My take: Regardless of the sceptics, it has to be acknowledged that Salesforce is an industry leader. Few, if any, companies in B2B tech have faced the same challenges of scaling beyond $30bn ARR. Benioff’s grand plan faces critical tones from investors, but it wouldn’t be the first time he proves them wrong.

🥹 The best of LinkedIn this week

➡️ How much is your share package worth at IPO? Great illustration here.

➡️ My controversial post on if Sales Engineers should be salesy or technical.

➡️ China vs. US. The chip wars continue.

➡️ European deep tech investment lags behind the rest of the wolrd.

➡️ Kyle Coleman gathers top 5 traits of successful sales leaders.

🗞️ In other news

Mind the talent gap

KPMG surveys execs on talent shortage and digital transformation. (article)

“This was followed by lack of skills to implement or fully take advantage of new systems (29pc), sub-optimal data management (28pc) and a risk-averse corporate culture that is slow to embrace change and disruption (24pc).”

👉 My take: It’s never been a better time to work in tech. Execs are investing in digital transformation and are unable to reap more value from the investment due to talent shortage.

Tech consolidation is top of mind

Battery Ventures released its Cloud Quarterly report (here). Some relevant insights on how GTM leaders should approach the current climate and drive efficiency.

👉 My take: Sales leaders must look at the end-to-end customer experience, not just the new logo land. In most tech companies, the value is realised post-signature, and tight monitoring of usage metrics is critical.

🙏 That’s it. Thank you for reading.

🤓 Don’t know me? Here’s the about section.

My name is Semir Jahic. I’m a self-confessed news junkie, and I’m also a student of startups and obsessed with what it takes to build something of value.

In More Value, I’ll share what I’m reading, learning, and observing to help you create more value.

More value is for go-to-market professionals in Sales, Customer Success, Delivery and anywhere else in the enterprise software industry.

If that’s you, subscribe.